It’s widely known that insurance reimbursements are compressing. Medical credit is tightening. And private equity-backed DSO operators are finally turning a hard eye toward patient financing, and not liking what they see.

Here's what the conversation actually sounds like in portfolio reviews right now:

"You're sitting on deferred cash tied up in payment plans. We need that capital working harder."

"Bad debt is running at 10%. We've got 25 people in Rev Cycle chasing receivables."

"96% of our financing is going through one lender. We're converting 25% of those applications. That's not a strategy."

These aren't edge cases. They're the norm.

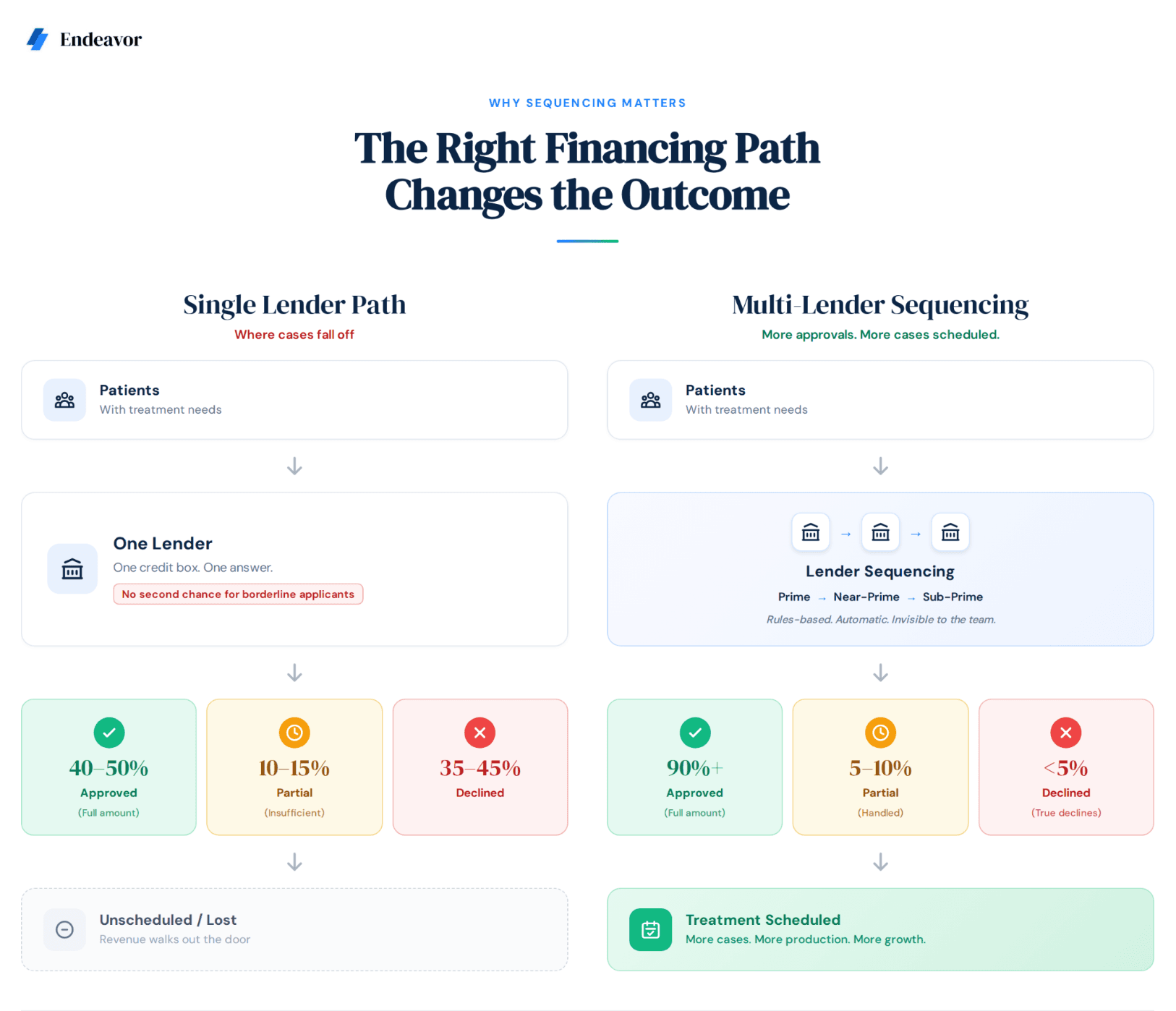

The single-lender problem is bigger than most operators realize

Most specialty practices today run patient financing through two or three prime lenders.

Someone has told them they’ll see a high approval rate with a prime lender. But this strategy is quietly limiting who gets approved and at what amount. More importantly, the partial fills are affecting conversion.

Every lender has a "credit box" — its own thresholds around credit score, debt-to-income ratio, and risk tolerance. A decline from one lender doesn't mean a patient is unfinanceable. It means that lender said no.

The breakdown by credit tier:

-

Prime (720+ score) — MDRs as low as 3–4%. Where most legacy lenders, including CareCredit, compete almost exclusively.

-

Near Prime (620–720) — The largest segment of declined patients. MDRs typically 7–10%.

-

Sub Prime (below 620) — Higher MDRs (15–20%), but strong approval rates on full treatment amounts are still achievable.

One leading lender declines nearly $20 billion in loan requests annually.

Most of that volume doesn't disappear — it walks out the door of a practice that had no second option ready.

The partial fill problem compounds it

A patient needs $12,000 of implant work. They're approved for $4,000. The case doesn't close. The practice logs it as a soft decline and moves on.

This is called a partial fill — one of the most common reasons financed cases don't convert, even when a lender technically said yes.

At scale, the math becomes material fast:

-

1,000 ortho starts per month across 50 locations

-

A 10% partial-fill rate = 100 cases per month that almost closed

-

Annualized, that's 1,200 cases sitting in a blind spot on the P&L

What PE is actually asking for

When we talk to PE-backed operators, the ask isn't complicated. It's usually some version of:

-

Reduce bad debt exposure without growing the collections team

-

Pull cash forward from long-dated in-house payment plans

-

Improve case acceptance without adding marketing spend or headcount

-

Get visibility into diagnosed-but-unscheduled patients who were never offered financing

The problem is that the infrastructure at most portfolio companies isn't built to deliver any of that. A single prime lender, a front desk team without standardized financing workflows, and no consistent approach across locations — that combination puts a hard ceiling on performance.

What better looks like

Practices that have moved to a tiered, multi-lender model — where prime lenders are evaluated first and applications automatically cascade into near-prime or sub-prime options — are seeing accommodation rates move from the 40–50% range to 75%+.

The operational gains compound from there:

-

Third-party lenders fund within 72 hours vs. 12–24 months on internal payment plans

-

Credit risk shifts off the practice's balance sheet

-

Collections headcount pressure eases

-

Capital is freed up to reinvest in growth

As one DSO CFO recently told us: "If we could find something that matches our bad debt experience and saves us on the collections side — I don't know how many people we have doing that, but it's probably 50 plus — that would be the win."

The bottom line

Patient financing rarely makes it onto the critical path in PE diligence. It probably should.

For most dental platforms, it's an undermanaged lever sitting between current performance and what the portfolio could actually generate — with no additional acquisition spend required.

The cases aren't lost because patients can't afford treatment. They're lost because the workflow wasn't built to find the right approval path at the right moment. That's a solvable problem.