If you are running a dental or medical practice and you are still relying on one or two lenders to handle your patient financing, I want to walk you through what that is actually costing you. Not in abstract terms — in patients who left your chair without getting the treatment they needed, and revenue that quietly walked out your door.

I have spent the better part of a decade in medical and dental finance, and I have watched this pattern repeat itself across hundreds of practices.

A treatment coordinator presents financing, the patient applies, and if that one lender declines them, the conversation is over. Or best case scenario, the coordinator tries a second lender. But often another Prime Lending option that has much the same “buy box” as the first. Maybe they don’t even bother. Either way, a patient who needed care goes without it and a practice that could have grown its revenue did not.

There is a better way. It is called an aggregator model, and it changes the outcome for the patient, the practice, and the lender.

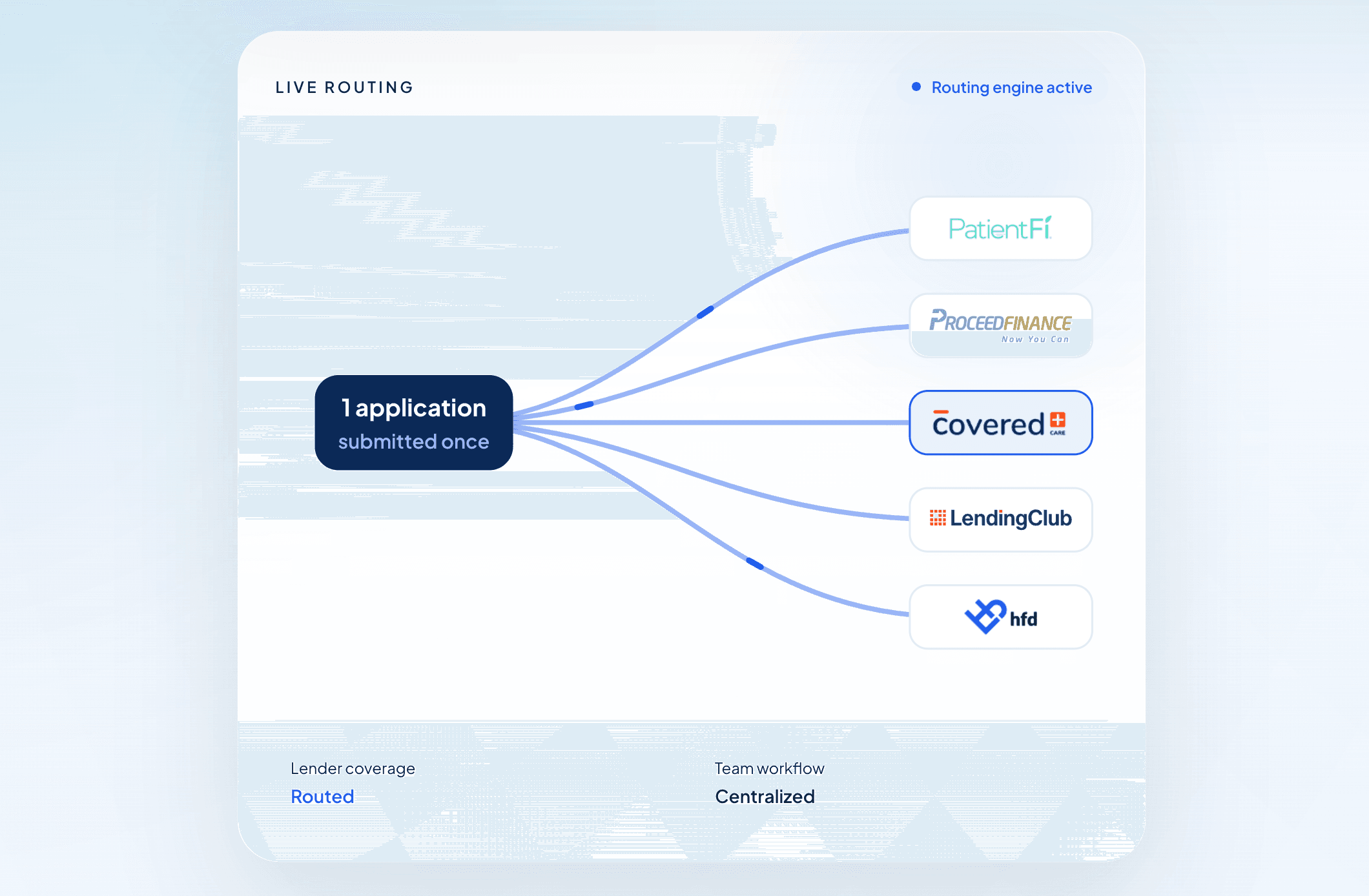

One Application. Every Lender. The Best Offer.

The core idea is simple. Instead of a patient applying to one lender and hoping, they submit a single application that is evaluated across multiple lenders — at every tier of the credit spectrum. Prime lenders. Near-prime lenders. Subprime lenders. The platform's logic then surfaces the best offer available for that patient, given their credit profile.

This matters because credit is not binary. A patient who does not qualify with a prime lender may qualify beautifully with a near-prime lender at a rate that still works for them. A patient with a more challenged credit history may still find an option in the subprime tier. The goal is to have coverage at each tier — ideally one or two strong lenders per band — so that the widest possible range of patients sees a "Congratulations" screen when they apply.

For example, in the platform I work with today, I routinely see offer rates between 85% and 95% in an industry like Ortho. That means up to 95 out of 100 patients who apply receive an offer. Compare that to a single-lender approach where you might approve 40% to 60% of applicants on a good day, and the difference becomes impossible to ignore.

What Typically Happens Without an Aggregator

In most practices I encounter, the financing workflow looks something like this: the treatment coordinator presents one or two prime lenders. If the patient is declined, they might try a second prime lender. If they are declined again, the conversation usually ends there.

The problem is that sending a patient to two or three prime lenders in succession is not just inefficient — it can actually hurt the patient. Some lenders still use hard credit inquiries in a short window can lower their credit score and reduce their chances of qualifying with anyone. You have not helped them. You have made things harder for them.

An aggregator solves this by submitting one application using only lenders that leverage a “soft inquiry” to evaluate credit and then letting the platform intelligently route across lenders behind the scenes. The patient's credit is only impacted if they choose to move forward. The logic does the work. The best available offer comes forward.

The Training Problem — and Why It Matters More Than You Think

Here is something that rarely gets talked about: the biggest barrier to patient financing is not the credit. It is the treatment coordinator.

I do not mean that as a criticism. I mean it as a structural observation. When a practice is working with three or four different lenders, that means three or four different portals, three or four different applications, three or four sets of processes and approval flows. Asking a treatment coordinator — who is also managing schedules, handling patient questions, coordinating with the clinical team, and doing a dozen other things — to master all of that is asking too much.

What typically happens is one of two things. Either the coordinator learns one lender well and defaults to it for everyone, missing the patients who might have qualified elsewhere. Or they become so uncertain about the process that they stop proactively offering financing at all. Both outcomes are bad for the patient and bad for the practice.

An aggregator changes this entirely. One portal. One application. One process to learn. When a treatment coordinator knows exactly what to do and feels confident doing it, they offer financing more consistently. When they offer financing more consistently, more patients hear about it. When more patients hear about it, more patients apply. And when more patients apply through a platform with strong offer rates, more patients get approved.

That chain of events — confidence leading to consistency leading to volume leading to approvals — is where the real growth is hiding in most dental practices.

Everyone Wins

I want to be clear that the aggregator model is not just good for practices. It is good for patients, and it is good for lenders.

For patients, it means they are treated with dignity. They apply once. They get the best offer available to them. They are not bounced between portals or hit with multiple hard inquiries. They leave the practice knowing they have a real path to getting the care they need.

For lenders, it means they are matched to the patients who fit their credit box — not force-fit into approvals they were never built to handle. A subprime lender gets subprime applicants. A prime lender gets prime applicants. Everyone is working in their lane, and the quality of paper reflects that.

And for the practice, the math is straightforward. More approvals mean more case acceptance. More case acceptance means more revenue. More revenue means a healthier practice that can invest in its team, its technology, and its patients.

The dental practices that figure this out first will have a significant advantage over those that do not. The question is not whether the aggregator model works. I have seen the numbers. It works. The question is how long you are willing to wait before you give your patients — and your practice — the benefit of it.